How Online Income Reduces Financial Anxiety for Good

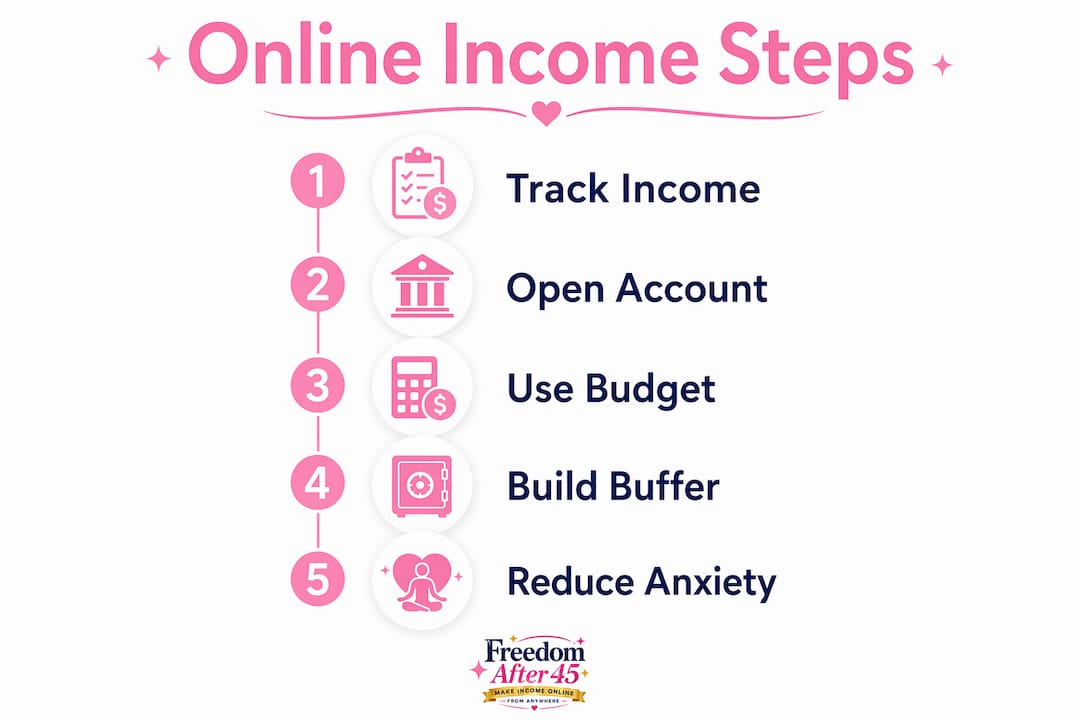

Financial anxiety is a chronic stress response triggered by perceived loss of control over money. Understanding how online income reduces financial anxiety starts with one fact: a side hustle brings in an average of nearly $1,000 per month, giving households real breathing room on bills, debt, and savings. That breathing room is not just financial. It is neurological. When your brain stops scanning for financial threats, your entire mental load drops. The 70/20/10 allocation rule and zero-based budgeting are two frameworks that turn irregular online earnings into a predictable system, and predictability is the direct antidote to money-driven anxiety.

How online income reduces financial anxiety compared to a single paycheck

A single paycheck creates a single point of failure. When that income shrinks or disappears, the nervous system reads it as a threat. Diversifying online income streams across freelancing, digital products, and affiliate channels removes that single point of failure. The result is a psychological shift from scarcity to control.

Online income also offers structural advantages that a traditional job cannot match:

- Account separation reduces decision fatigue. Separating business and personal accounts frees cognitive resources and lowers daily financial anxiety for solopreneurs. When you stop mixing funds, you stop second-guessing every purchase.

- Income smoothing counters feast-and-famine cycles. Online earners who use a buffer account to absorb high-income months and fund low-income months report far less emotional volatility around money.

- Multiple income streams build resilience. Treating online income as an ecosystem of smaller, reliable sources means one stream drying up does not collapse the whole system.

Pro Tip: Open a dedicated business checking account the day you earn your first dollar online. That single structural move reduces financial confusion and the anxiety that comes with it.

The psychological benefit here is not subtle. Financial anxiety triggers the nervous system’s threat response. Predictable financial systems create calm confidence and reduce mental load. Online income, when structured correctly, creates exactly that predictability.

How to use budgeting frameworks to turn online income into calm

Budgeting is the mechanism that converts raw online earnings into anxiety relief. Without a framework, even a good income month feels chaotic. With one, even a lean month feels manageable.

Three frameworks work best for online earners:

- Apply the 70/20/10 rule. The 70/20/10 allocation rule assigns 70% of income to essentials, 20% to goals and investment, and 10% to discretionary spending. This structure removes the guilt and second-guessing that fuel financial anxiety.

- Use zero-based budgeting. Zero-based budgeting assigns every dollar a specific job before the month begins. No dollar sits unaccounted for. That clarity eliminates the mental noise of wondering where money went.

- Calculate your Minimum Viable Income (MVI). Your MVI is the exact dollar amount that covers all personal and business costs without touching credit. Knowing this number gives you a clear financial floor. Anything above it is progress, not pressure.

| Framework | Core mechanism | Anxiety benefit |

|---|---|---|

| 70/20/10 rule | Allocates income by category | Removes guilt over spending |

| Zero-based budgeting | Assigns every dollar a job | Eliminates financial guessing |

| Minimum Viable Income | Sets a clear expense floor | Creates psychological safety |

Pro Tip: Calculate your MVI before your first full month of online income. Write the number down. Seeing a concrete floor removes the vague dread that makes financial anxiety so persistent.

Eliminating money stress is about creating mental space to plan achievable goals, not about reaching a specific wealth level. Precise budgeting is the tool that creates that space. These three frameworks work together: the 70/20/10 rule gives your income a shape, zero-based budgeting gives every dollar a purpose, and MVI gives you a floor to stand on.

Why financial buffers are the real cure for income-related stress

A buffer account is the single most effective tool for reducing anxiety in online earners. The concept is simple. Think of it as a water tank. Feast months fill the tank and lean months draw from it. Your monthly spending stays level regardless of what the income side does.

“The buffer is not a savings account. It is a shock absorber. Its only job is to make your financial life feel the same every month, no matter what your income does.”

Experts recommend that online earners build a buffer covering 6–12 months of combined business and personal expenses. That is a larger target than the traditional 3–6 month emergency fund advice. The reason is simple: irregular income creates irregular risk, and the buffer must match the risk.

| Buffer size | Best for | Anxiety reduction level |

|---|---|---|

| 3–6 months | Stable part-time online earners | Moderate |

| 6–12 months | Full-time or sole-income online earners | High |

The neuroscience behind this is direct. Stable passive income lowers amygdala activation and daily stress markers. The amygdala is the brain’s threat-detection center. When your buffer account removes the threat of a lean month, your amygdala quiets down. Chronic stress markers drop. You sleep better, think more clearly, and make better financial decisions. The buffer does not just protect your bank account. It protects your mental health.

Psychological and community strategies that multiply the effect

Financial tools work best when paired with behavioral habits. The most effective online earners combine budgeting frameworks with regular mental check-ins and peer support.

- Schedule monthly money dates. Set aside 30 minutes each month to review income, expenses, and buffer levels. Treating this as a scheduled appointment removes the avoidance behavior that lets anxiety build silently.

- Join a peer support group or mastermind network. Isolation amplifies financial anxiety. Connecting with other online earners normalizes income variability and provides practical advice from people facing the same challenges.

- Automate financial habits with technology. Apps like YNAB (You Need a Budget) and tools built into most business banking platforms can auto-transfer a set percentage of each payment into your buffer account. Automation removes the willpower requirement from saving.

- Track income trends, not just totals. Watching a 3-month rolling average of your online income is more calming than watching a single month’s number. Trends reveal stability that individual months hide.

- Celebrate MVI milestones. When your buffer reaches one month of MVI coverage, mark it. When it reaches three months, mark it again. Positive reinforcement builds the financial confidence that anxiety erodes.

Even moderate passive income yields measurable reductions in stress biomarkers. That means you do not need to replace your full salary before you feel relief. Small, consistent online income paired with these behavioral habits creates a compounding effect on mental well-being.

Key Takeaways

Online income reduces financial anxiety most effectively when paired with structured budgeting, a 6–12 month buffer account, and consistent behavioral habits that reinforce financial control.

| Point | Details |

|---|---|

| Income diversification reduces risk | Multiple online income streams prevent a single source from collapsing your finances. |

| 70/20/10 rule removes spending guilt | Allocating income by category gives every dollar a purpose and calms anxious thought patterns. |

| Buffer accounts stabilize mental health | A 6–12 month buffer absorbs income swings and lowers amygdala-driven stress responses. |

| Zero-based budgeting eliminates guessing | Assigning every dollar a job before the month starts removes the mental noise of untracked spending. |

| Behavioral habits compound the benefit | Monthly money reviews and peer support reinforce the financial confidence that anxiety erodes. |

What I have learned from watching online income change lives

Financial anxiety is not a character flaw. It is a predictable response to unpredictability. I have seen this pattern repeat across thousands of women who came to Freedom After 45 carrying real fear: fear of a lean month, fear of a medical bill, fear of outliving their savings. What changed their relationship with money was not a windfall. It was structure.

The insight most people miss is that the anxiety does not disappear when the income goes up. It disappears when the system goes in. I have watched women earning $300 a month online feel calmer than women earning $3,000 a month with no framework. The $300 earner knew exactly where every dollar went. The $3,000 earner was still guessing.

The other thing I have noticed is that over 40% of side hustlers earn $100 or less per month at the start. That number sounds discouraging until you realize that $100 a month, properly allocated, can fully fund a starter buffer in 12 months. Small income, structured correctly, is not a consolation prize. It is a foundation.

The mindset shift from scarcity to control is the real product of online income. Money is the vehicle. Control is the destination. Once you feel control, the anxiety loses its grip.

— Freedom After 45

A practical next step for women ready to build that control

Financial anxiety shrinks when income becomes predictable. Freedom After 45 built the 2-Hour Workflow specifically for women over 45 who want daily income without needing a social media following, an existing product, or technical skills.

The program delivers a step-by-step blueprint for generating $100 to $1,400 per day by committing just two hours a day. Thousands of families have already used it to build the kind of financial floor that makes anxiety optional. The workflow is designed to be started immediately, with no prior experience required. If the frameworks in this article resonated with you, the next logical step is putting them into practice with a system that handles the structure for you.

FAQ

How quickly does online income reduce financial anxiety?

Even moderate passive income produces measurable reductions in stress biomarkers. Most online earners report noticeable relief once they have one month of MVI coverage in a buffer account.

What is the best budgeting rule for irregular online income?

The 70/20/10 rule works well for most online earners because it allocates income by category rather than fixed dollar amounts. It scales up and down with income variability without requiring a full budget rebuild each month.

How large should an emergency buffer be for online earners?

Experts recommend a buffer covering 6–12 months of combined business and personal expenses. This is larger than the standard advice because online income cycles carry more variability than a salaried paycheck.

Does separating business and personal accounts really help with anxiety?

Yes. Separating accounts reduces decision fatigue and frees cognitive resources. When funds are mixed, every purchase triggers a mental calculation that compounds daily stress.

Can a small online income still reduce financial stress?

A side hustle averaging close to $1,000 per month provides real breathing room, but even $100 per month, allocated correctly into a buffer, builds measurable financial safety over time.