Why Student Debt Makes Online Income Critical in 2026

Student debt is the single biggest reason income diversification has shifted from a nice idea to a financial necessity for millions of Americans. The average borrower carries a monthly payment that competes directly with rent, groceries, and basic savings. For those in the Gen Z bracket, monthly loan payments average $526, nearly double the all-age average of $284. A single paycheck from a traditional job rarely covers that payment and leaves room for anything else. That gap is exactly why student debt makes online income critical, and why income diversification has become the defining financial strategy of this decade.

Why student debt makes online income critical for financial stability

The real damage from student debt is not just the dollar amount. It is the compounding pressure that reshapes every financial decision a borrower makes for years after graduation.

The mental and financial toll of high loan payments

61% of borrowers experience significant stress or anxiety tied directly to their student debt. That statistic matters because financial stress does not stay in a spreadsheet. It affects sleep, career decisions, relationships, and the ability to think clearly about money. The same research shows that 84% of borrowers delay major life milestones, including home ownership and starting a business, because of loan obligations. Debt does not just drain a bank account. It drains ambition.

The financial math is equally punishing. When $526 leaves your account every month before you have paid for anything else, the margin for saving, investing, or building a buffer shrinks to almost nothing. 58.3% of borrowers prioritize bills over saving, which means they are perpetually one unexpected expense away from a financial crisis. A single income source cannot absorb that kind of pressure reliably.

- Gen Z borrowers pay an average of $526 per month in student loan payments

- 84% delay milestones like home ownership or starting a business

- 61% report significant stress or anxiety from debt

- 58.3% consistently prioritize bills over building savings

- 81.3% name reduced stress as their primary financial freedom goal

The pattern is clear. High debt payments force a reactive financial posture. Online income creates a proactive one.

What is the modern earner economy, and why does it matter?

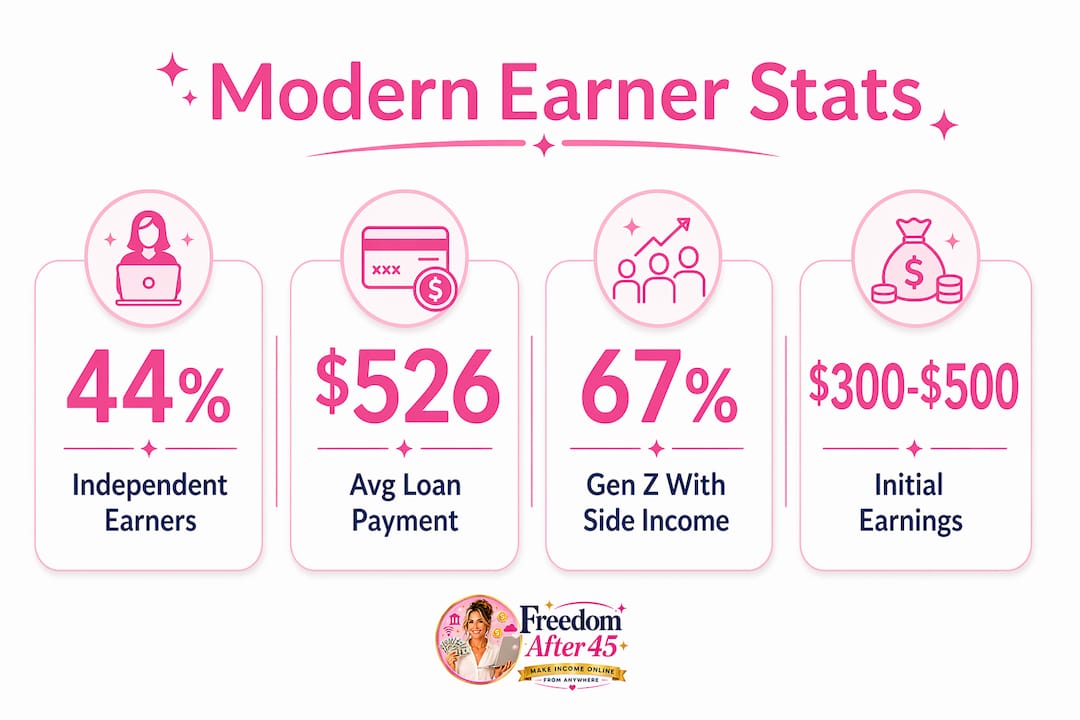

The modern earner economy is defined by individuals who generate income from multiple, often digital, sources rather than relying on a single employer paycheck. This is not a fringe trend. Independent income earners grew 30% between 2024 and 2026, reaching 54 million people in the United States. That growth reflects a structural shift in how Americans earn, not just a temporary response to economic uncertainty.

The same data shows that 44% of wage earners now hold at least one independent income source, and the average modern earner manages 2.7 payment channels simultaneously. Managing multiple income streams sounds complicated, but it is actually a form of financial defense. If one channel slows down, the others keep cash flowing.

Common online income streams worth knowing

The most accessible online income paths fall into a few clear categories:

- Freelancing: Writing, graphic design, web development, and virtual assistance through platforms like Upwork or direct client relationships

- Content creation: YouTube channels, newsletters, and niche blogs that generate ad revenue or sponsorships over time

- Digital products: E-books, templates, courses, and printables that sell repeatedly without ongoing labor

- Tutoring and coaching: Subject-specific tutoring or skill coaching delivered via video call

- Gig economy work: Task-based income from platforms that pay per completed job

Each of these removes the single-paycheck dependency that makes student debt so suffocating. 67% of Gen Z borrowers say having multiple income streams is not optional. It is essential for financial security.

| Income type | Startup cost | Time to first income | Scalability |

|---|---|---|---|

| Freelancing | Low | Days to weeks | Moderate |

| Digital products | Low to medium | Weeks to months | High |

| Content creation | Low | Months | High |

| Tutoring or coaching | Minimal | Days | Moderate |

Which online income methods actually work for managing debt?

Not every online income path is worth your time. The importance of online income lies in choosing methods that build real, compounding value rather than chasing fast money that evaporates.

Methods that deliver real returns

Tutoring, freelance writing, and niche content creation consistently rank as the most viable starting points. Initial online earnings typically range from $100 to $600 per month, but that figure compounds three to five times over two to three years as skills sharpen and reputation builds. Starting early matters more than starting perfectly. A freelance writer who begins with $200 per month and grows consistently will outperform someone who waits for the “right” opportunity.

Digital products deserve special attention because they separate your income from your hours. A well-researched template or guide can sell hundreds of times without additional work. That is the kind of income that actually moves the needle on a $526 monthly loan payment.

Pro Tip: Start with one income stream, reach $300–$500 per month in consistent earnings, then add a second. Spreading attention across five methods from day one produces mediocre results in all of them.

Pitfalls that waste time and money

Experts consistently warn that some online income courses exploit debt anxiety by promising fast returns through trading, crypto flipping, or MLM structures. These approaches rarely deliver predictable income and often cost more than they return. Freelancing and digital product creation offer far more reliable results because they are built on solving real problems for real people. The rule is simple: if an income method requires you to recruit others or buy inventory upfront, walk away.

- Freelance writing or editing: Low barrier, immediate market demand, and skills that compound with practice

- Niche content creation: Pick a specific topic, build an audience, and monetize through ads or affiliate arrangements

- Online tutoring: High hourly rates relative to effort, especially in math, science, and test preparation

- Digital product sales: Create once, sell repeatedly, with no inventory or shipping costs

- Virtual assistance: Administrative and organizational skills translate directly to remote client work

Sustainable online income comes from creating genuine value, not chasing shortcuts. That principle separates people who build lasting financial agency from those who spin their wheels.

How to balance online income with student debt repayment

Earning more money only helps if you deploy it correctly. The impact of student loans extends beyond the monthly payment. It shapes how you should think about every dollar of extra income you generate.

The interest rate decision

The math on extra income is straightforward. When your loan interest rate sits below 5%, investing extra income in index funds or retirement accounts typically produces better long-term results than accelerating principal payments. When rates exceed 7%, aggressive principal reduction wins. Knowing your exact rate before deciding where extra income goes is not optional. It is the foundation of a sound repayment strategy.

Protecting your loan benefits

Accelerating repayment without checking your loan terms can cost you thousands in forfeited benefits. Programs like Public Service Loan Forgiveness (PSLF) and Income-Driven Repayment (IDR) plans reward borrowers who make consistent, qualifying payments over time. Paying extra on a loan that qualifies for PSLF does not accelerate forgiveness. It just reduces the balance you would have had forgiven anyway. Always verify your loan terms at studentaid.gov before routing extra income toward principal.

Pro Tip: Treat loan forgiveness programs as a financial asset, not a fallback. If you qualify for PSLF, the math almost always favors making minimum payments and investing the difference.

- Know your exact interest rate before deciding how to use extra income

- Check whether your loans qualify for PSLF or IDR before making extra payments

- Build a $500–$1,000 emergency buffer before accelerating any debt repayment

- Use income-driven repayment to keep minimum payments manageable while building online income

Building an emergency buffer of $500 to $1,000 before aggressive repayment is not optional. Without it, one car repair or medical bill forces you onto a high-interest credit card, which erases weeks of repayment progress instantly.

Key Takeaways

Student debt makes online income critical because a single paycheck cannot reliably cover high loan payments, living expenses, and savings simultaneously. Income diversification is the most direct path to financial stability and debt freedom.

| Point | Details |

|---|---|

| Debt pressure is real and measurable | Gen Z borrowers pay $526 per month on average, nearly double the all-age average. |

| Multiple income streams are now standard | 54 million Americans earn independently, with the average earner managing 2.7 payment channels. |

| Start simple and compound over time | Initial online earnings of $100–$600 per month can grow three to five times within a few years. |

| Match repayment strategy to interest rate | Rates below 5% favor investing; rates above 7% justify aggressive principal reduction. |

| Protect loan benefits before paying extra | PSLF and IDR plans can be worth more than accelerated payments. Always check studentaid.gov first. |

The real reason online income changes everything about debt

At Freedom After 45, the conversation about debt and income comes up constantly. What strikes me most is not the dollar amounts. It is how quickly a second income stream shifts someone’s entire relationship with money.

Borrowers who rely on one paycheck live in a reactive state. Every financial decision is made under pressure, which means most decisions are made poorly. Adding even $300 per month from an online source changes the psychology completely. Suddenly there is room to think, to plan, and to make choices based on long-term goals rather than immediate survival.

The market trend I find most telling is that online income creates financial agency that debt repayment alone never can. Paying down a loan reduces a liability. Building an income stream creates an asset. Those are fundamentally different moves, and the people who understand that distinction reach financial freedom years ahead of those who do not.

The pitfall I see most often is people waiting until they feel “ready” to start. There is no ready. There is only starting with what you have and improving from there. The compounding effect of early online income is real. A year of consistent effort at $200 per month beats six months of intense effort at $600 per month because the habits, skills, and client relationships built in year one carry forward indefinitely.

— Freedom After 45

A practical system for earning online while managing debt

Knowing that online income matters is one thing. Having a clear, repeatable system to generate it is another.

Freedom After 45 built the 2-Hour Workflow specifically for people who need real income without complicated setups or prior experience. The program teaches a daily process that generates $100 to $1,400 in profit, working just two hours a day. No social media following required. No product inventory. No technical background needed. Thousands of families have used this method to create consistent income that runs alongside their existing financial obligations. For anyone carrying student debt and looking for a structured, proven path to supplemental income, this is where to start.

FAQ

What is the average monthly student loan payment in 2026?

Gen Z borrowers pay an average of $526 per month on student loans, nearly double the all-age average of $284. That gap makes supplemental income a practical necessity rather than a luxury.

How much can you realistically earn from online income as a beginner?

Initial online earnings typically range from $100 to $600 per month. With consistent effort, that figure compounds three to five times over two to three years as skills and reputation grow.

Should I pay off student loans faster or invest extra income?

The answer depends on your interest rate. Rates below 5% generally favor investing; rates above 7% justify accelerating principal payments. Always check your specific loan terms at studentaid.gov before deciding.

What online income methods work best for debt-burdened individuals?

Freelance writing, online tutoring, digital product creation, and niche content creation offer the most reliable returns. These methods build real skills and compound in value over time without requiring upfront capital.

Can online income reduce the stress caused by student debt?

Yes. Research shows that 61% of borrowers experience significant debt-related anxiety. Adding a second income stream creates financial breathing room, which directly reduces the psychological pressure that debt creates.