How Online Income Builds Student Financial Habits

Earning money online is the fastest path students have to develop real financial habits before graduation. How online income builds student financial habits comes down to one mechanism: irregular earnings force you to budget, track, and plan in ways a fixed allowance never demands. Students who manage their own income streams learn the 55/30/15 budgeting rule, build emergency cushion accounts, and practice habit stacking long before their peers enter the workforce. The result is measurable financial literacy, not just extra spending money.

How online income builds student financial habits from day one

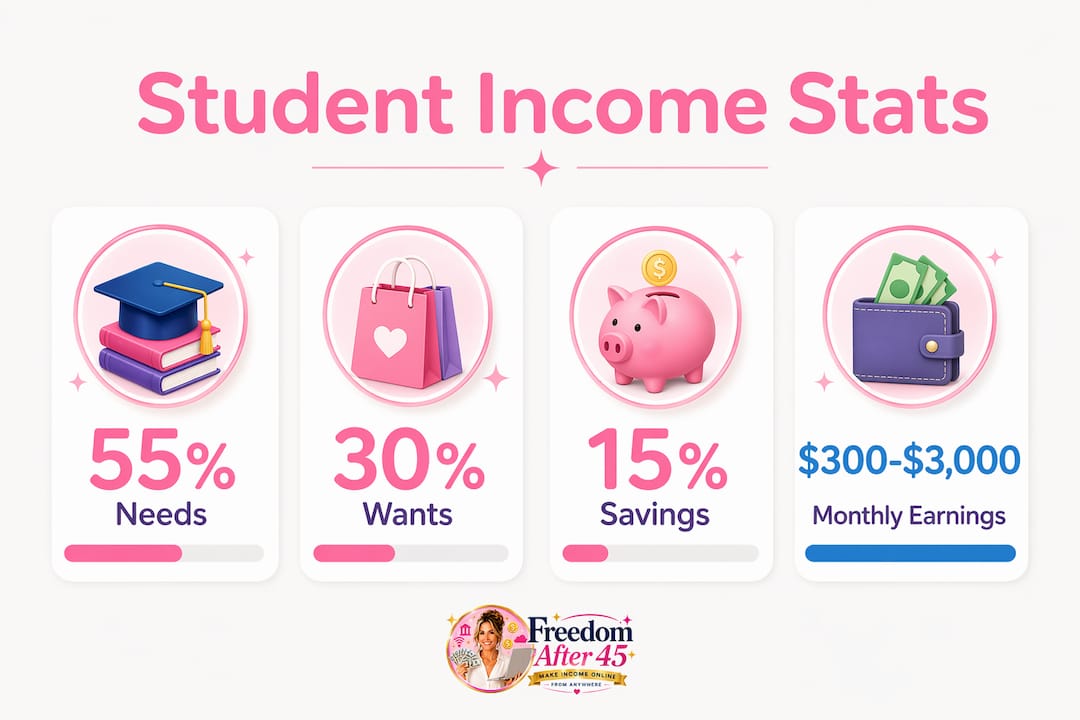

The most accessible online income streams for students fall into four categories: AI micro-tasking, freelancing, online tutoring, and digital product sales. Each one teaches a different financial skill at a different pace. Students can realistically earn $300–$3,000 per month through these channels, depending on hours invested and skill level. That range matters because it reflects real variability, and variability is exactly what forces financial discipline.

AI micro-tasking platforms pay within days and require almost no setup. Freelancing and tutoring take weeks to build consistent clients but generate higher hourly rates. Digital product sales, such as selling study guides or Canva templates, require upfront effort but can produce passive returns over time. Each model demands a different relationship with money.

| Income stream | Startup time | Typical monthly range | Core skill built |

|---|---|---|---|

| AI micro-tasking | 1–3 days | $100–$500 | Speed and consistency |

| Freelancing | 2–6 weeks | $300–$2,000 | Client management |

| Online tutoring | 1–2 weeks | $200–$1,500 | Communication |

| Digital product sales | 2–4 weeks | $50–$3,000 | Long-term thinking |

Pro Tip: Start with one income stream and master its payment cycle before adding a second. Understanding when money arrives is the first step to budgeting it correctly.

The skill-building aspect of online work is not incidental. Every hour spent delivering a freelance project or tutoring a student is an hour spent learning that income is earned, not given. That mindset shift is the foundation of every strong financial habit that follows.

How does online income help students budget and manage money?

Fixed costs consume 70–80% of monthly income for most students. That reality makes the standard 50/30/20 budgeting rule impractical. A modified 55/30/15 split works better: 55% for needs, 30% for wants, and 15% for financial goals and buffers. The 15% savings category is the critical piece because it forces students to treat saving as non-negotiable, not optional.

Managing irregular income adds another layer of complexity. A student who earns $800 one month and $300 the next cannot budget the same way each time. The solution is a cushion account approach: deposit all earnings into a buffer account, then pay yourself a fixed monthly “salary” from it. This smooths out income spikes and prevents the lifestyle inflation that kills budgets when a good month arrives.

| Budget category | Percentage | Typical student expense |

|---|---|---|

| Needs | 55% | Rent, groceries, transportation |

| Wants | 30% | Dining out, entertainment, clothing |

| Goals and buffers | 15% | Emergency fund, savings, skill investment |

Tracking expenses in real time catches what students call “budget leaks.” Forgotten digital subscriptions and small recurring charges aggregate to $60–$120 per month without students noticing. That is money that could fund a course, a software tool, or three months of an emergency buffer.

Budgets also need to flex. Constant adjustment aligned with income or expense changes prevents overspending and financial stress. A student who lands a bigger freelance project in march should revise their budget that week, not wait until the month ends.

Pro Tip: Run a subscription audit every 90 days. List every recurring charge, cancel anything unused, and redirect that money to your buffer account.

The discipline required to manage an online income budget is identical to the discipline required to manage a salary. Students who practice it now arrive at their first job already knowing how to allocate a paycheck.

What financial habits do students build through online work?

Habit stacking is the most effective technique for building lasting money habits. It means attaching a new financial behavior to an existing daily routine. For example, checking your bank balance every morning while drinking coffee turns financial awareness into an automatic act rather than a chore. Small, repeatable habits anchored to existing behavior outlast any restrictive budget plan.

Students who earn online also develop a clearer understanding of value exchange. Income is compensation for value delivered. That framing changes how students spend money because every purchase gets measured against the hours it took to earn it. A $60 impulse buy feels different when you know it cost four hours of tutoring work.

The most financially literate students reinvest early earnings rather than spending them immediately. Putting the first $200 of freelance income into a better microphone, a design course, or a faster laptop raises earning potential for every project that follows. Reinvesting earnings into skill-building accelerates income growth far more than spending that same money on consumption.

Impulsive online spending is the single biggest threat to student budgets. One proven method to reduce it: remove saved card data and disable one-click purchasing on every shopping platform. Introducing friction into the payment path forces a pause. That pause is often enough to cancel the purchase entirely.

“Effective money habits form not from restrictions but by attaching simple tasks to daily routines for consistency.”

Pro Tip: Set a 48-hour rule for any non-essential purchase over $30. Add it to a wishlist, wait two days, and buy it only if you still want it. Most of the time, you won’t.

These habits compound. A student who tracks spending, audits subscriptions, reinvests earnings, and pauses before buying arrives at graduation with financial behaviors that most adults spend years trying to build.

How does online income prepare students for life after graduation?

Online student workers develop remote collaboration skills, digital fluency, and project management experience that employers actively seek. Spending 5–15 hours per week on a side hustle translates directly into resume experience with measurable outcomes. A student who managed three freelance clients, delivered 20 projects, and earned $8,000 over two semesters has a concrete professional record before their first job interview.

The career advantage goes beyond the resume line. Students who manage their own income learn to communicate with clients, meet deadlines without supervision, and handle payment disputes. These are workplace skills that classroom coursework rarely teaches directly.

Competence before income is the principle that separates students who build lasting financial independence from those who chase quick wins. Skill-based earnings compound over time. A student who spends six months becoming genuinely good at video editing earns more per hour in month seven than in month one, and that trajectory continues after graduation.

The compounding effect applies to financial habits too. Students who practice budgeting irregular income, tracking expenses, and reinvesting earnings for two or three years develop an instinct for money management that shows up in every financial decision they make as adults. They negotiate salaries more confidently, avoid consumer debt more consistently, and build savings faster than peers who never managed their own income stream.

Key Takeaways

Online income builds student financial habits by creating real consequences for every financial decision, which no classroom exercise can replicate.

| Point | Details |

|---|---|

| Use the 55/30/15 rule | Allocate 55% to needs, 30% to wants, and 15% to savings and buffers. |

| Build a cushion account | Deposit all earnings into a buffer, then pay yourself a fixed monthly amount. |

| Practice habit stacking | Attach financial tracking to an existing daily routine to make it automatic. |

| Reinvest early earnings | Put first income into skills or tools, not consumption, to raise future earning potential. |

| Add friction to spending | Remove saved card data to pause impulsive purchases before they happen. |

What I’ve learned from watching students build income and habits at the same time

The students who make the most progress financially are not the ones who earn the most. They are the ones who treat their first $300 month as a financial system to manage, not a windfall to spend. That mindset is the real product of online income work.

The biggest mistake I see is treating online earnings as “extra” money with no budget rules attached. The moment income feels separate from your financial life, the habits stop forming. Every dollar earned online needs to go through the same budget categories as any other income. That discipline is what makes the habit stick.

Accountability tools matter more than motivation. Setting up automatic transfers to a savings account on the day income arrives removes the decision entirely. Pairing that with a weekly five-minute expense review creates a system that runs on structure, not willpower. Willpower runs out. Structure does not.

The students who build the strongest financial foundations are the ones who stay consistent through the low-earning months. A $200 month teaches more about budgeting than a $1,500 month because it forces real prioritization. That pressure is not a problem. It is the training.

— Freedom After 45

A proven workflow for building real online income

Building financial habits requires real income to practice with, and the right starting point makes all the difference.

Freedom After 45 offers a 2-Hour Workflow that teaches you how to earn 100% profit online daily without needing a social media following, an existing product, or prior experience. The program walks you through a step-by-step system that thousands of people have already used to create consistent, recurring income. For students who want to build financial habits on a real income foundation, this is a practical place to start. The skills you build through this workflow are the same ones that translate into long-term financial independence.

FAQ

What is the best budgeting rule for students with online income?

The 55/30/15 rule works better than the standard 50/30/20 split for students because fixed costs typically consume 70–80% of monthly income. Allocate 55% to needs, 30% to wants, and 15% to savings and financial goals.

How much can a student realistically earn online each month?

Students can earn between $300 and $3,000 per month through online income streams like freelancing, tutoring, AI micro-tasking, and digital product sales, depending on hours worked and skill level.

How does online work help with financial literacy for students?

Managing irregular online income teaches budgeting, expense tracking, and saving in real time. These are the core skills of financial literacy, and they develop faster through practice than through any course.

What is habit stacking and how does it apply to student finances?

Habit stacking means linking a new financial behavior to an existing daily routine, such as checking your bank balance every morning. This approach builds consistent money habits without relying on motivation or willpower.

How does online income experience help students after graduation?

Students who manage online income develop remote collaboration skills, project management experience, and a documented earnings record. These advantages show up directly on resumes and in salary negotiations.